You know what’s worse than being broke? Feeling like your money isn't working as hard as you do. Many of us are fed up with the limitations of traditional banking, where our hard-earned savings sit idle, earning mere crumbs in interest. But what if there was a way to break free and unlock the true potential of your wealth?

Enter the infinite banking Concept (IBC). This financial strategy offers a unique approach to banking that empowers you to take control of your finances and build wealth in a way that traditional banking cannot match.

But what exactly is this concept, and how can it benefit you? If you’ve heard the phrase “Be Your Own Bank” get thrown around but never really understood it, all that ends today. We'll explore what exactly infinite banking is, how it works, and most importantly, the pros and cons you need to consider before deciding if it's the right path for you.

What is Infinite Banking?

In simple terms, infinite banking is a concept that allows you to become your own banker. It involves using a participating whole life insurance policy as a financial tool to create a source of financing for yourself. Instead of relying on traditional banks for loans, you borrow against the cash value of your insurance policy, essentially borrowing from yourself.

It goes by many names: the ‘perpetual wealth code', ‘cashflow banking', or the ‘money multiplier'. But infinite banking hands you the power to borrow against yourself and grow your wealth on your terms. Note that you don't have to have a whole life policy, but it's the best one to use.

How Does Infinite Banking Work?

Here's a step-by-step breakdown of how infinite banking works:

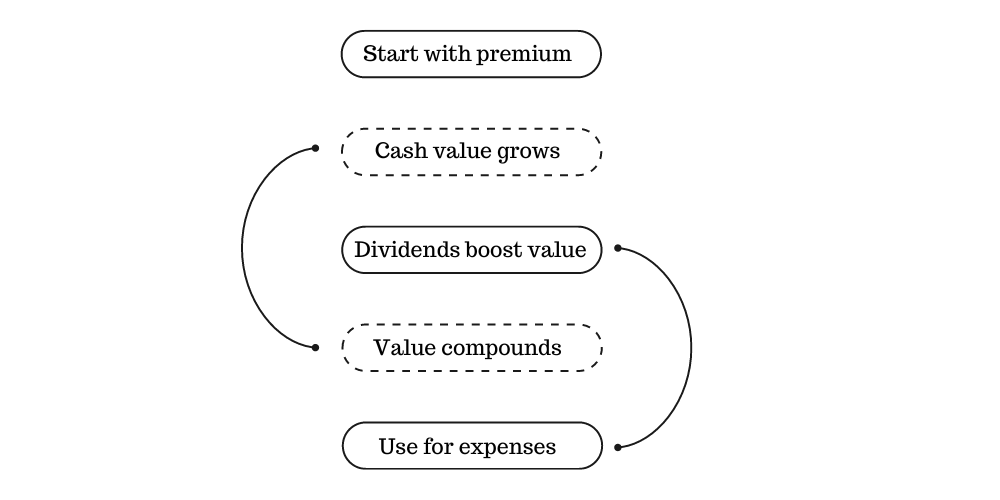

- Purchase a Whole Life Insurance Policy: The first step is to acquire a whole life insurance policy. This type of policy provides both a death benefit and a cash value component. The cash value grows over time, providing a source of funds that you can borrow against.

- Pay Premiums: You pay regular premiums to keep the policy active. These premiums are used to fund the death benefit and contribute to the cash value of the policy.

- Accumulate Cash Value: Over time, the cash value of your policy grows, thanks to the premiums you've paid and any dividends the insurance company has paid out.

- Borrow Against the Cash Value: Once your policy has accumulated enough cash value, you can borrow against it. This is where the “becoming your own banker” concept comes into play. You're essentially borrowing from yourself, using your policy as collateral.

- Repay the Loan (Optional): You have the option to repay the loan, with interest, or let it accrue. If you choose not to repay the loan, the outstanding balance will be deducted from the death benefit paid to your beneficiaries when you pass away.

Whole Life Insurance Explained

To grasp how infinite banking works, you’ll need to understand some key concepts related to whole life insurance:

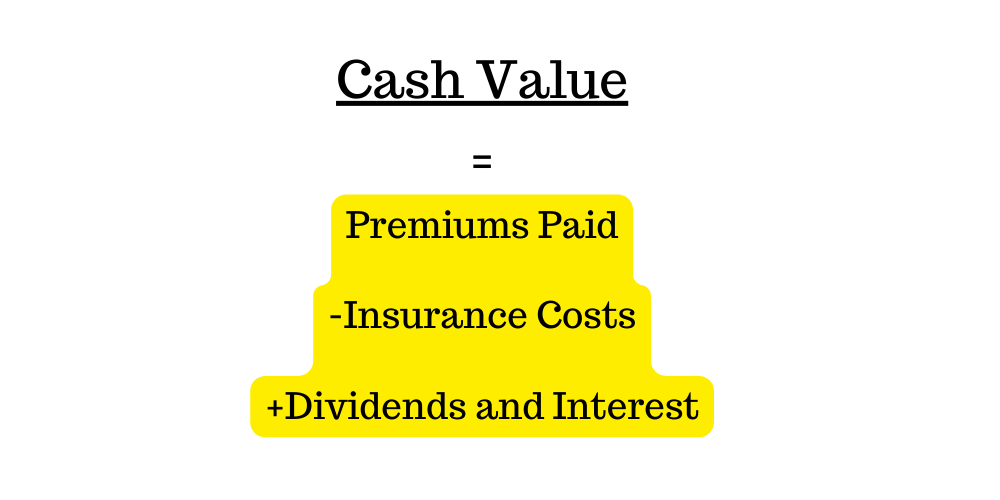

Cash Value

This is the accumulated money in your policy over time. It grows tax-deferred and can be accessed through policy loans.

Dividends

Some whole life policies are “participating,” meaning they pay dividends when the insurance company performs well. These dividends can increase the cash value of your policy.

Policy Loans/Borrowing

One of the key features of whole life insurance policies that enable infinite banking is being able to take out policy loans. Here's how it works:

- You borrow against the cash value of your policy.

- The loan is not taxable as income.

- The cash value continues to grow even as you borrow against it.

- You can repay the loan on your own schedule, with interest.

The key benefits of policy loans include:

- You're borrowing from yourself, so you're not subject to traditional lenders' restrictions or interest rates.

- The interest you pay on the loan goes back into your policy, further increasing your cash value.

- You have the flexibility to repay the loan on your terms, without penalty.

Pros and Cons of Infinite Banking

If it sounds too good to be true, it generally is. That's the mindset many people have when they first hear about infinite banking. They're intrigued by the promise of uninterrupted compounding and improved cash flow but cautious of opinions that suggest it might not be as beneficial as it seems. Statements like “You'd be using your own money” or “The commissions paid out are too high” can leave you feeling uncertain.

Understanding the full picture of infinite banking, including its pros and cons, is how you decide if this strategy is right for you. Before we go into the details, here’s a quick overview of the main benefits and drawbacks at a glance.

| Pros of infinite banking | Cons of infinite banking |

| Uninterrupted Compounding | Long-Term Commitment |

| Improved Cash Flow | Affordability Concerns |

| Flexibility and Control | Opportunity Cost |

| Tax-Free Loans | Lack of Liquidity |

| Guaranteed Death Benefit | Potential for Lower Returns |

| Risk Mitigation |

Infinite Banking Pros

Uninterrupted Compounding

Imagine being able to make significant purchases like cars or real estate investments while still allowing your cash value to grow. With infinite banking, you can do just that, leaving your money to continue working for you and exponentially increasing your net worth over time.

Improved Cash Flow

With infinite banking, your whole life insurance policy serves as a second source of income. Whether you face unexpected expenses or lose your primary source of income, you can tap into your policy's cash value to maintain financial stability without relying on traditional lenders. Our financial education courses equip you with the knowledge and tools to optimize your cash flow management, so you're prepared for any financial situation.

Flexibility and Control

One of the most significant advantages of infinite banking is the level of control it affords you. As your own banker, you are free to set the terms of your loans, including repayment schedules and interest rates. This flexibility allows you to tailor your financial strategy to meet your specific needs and goals.

Tax-Free Loans

Unlike traditional loans, self-issued loans from your infinite banking policy are not considered taxable income. This means you can access your cash value without worrying about additional tax liabilities, providing you with a tax-efficient way to finance major expenses or investments.

Guaranteed Death Benefit

You can enjoy the benefits of borrowing against your policy's cash value while still ensuring financial protection for your loved ones. The death benefit of your whole life insurance policy is guaranteed, meaning your beneficiaries will receive a payout regardless of any outstanding loans or withdrawals you've made during your lifetime.

Risk Mitigation

While no investment strategy is entirely risk-free, infinite banking offers a relatively low-risk approach to building wealth because it is an uncorrelated asset. Your insurance policy earns its guaranteed interest rates + dividends, which do not correlate with the stock market. So you need not fear what a repeat of 2008 or 2000 could do to your finances! If the stock market crashes, your little “bank” won't be affected at all.

As enticing as infinite banking may seem, you’ll need to weigh its potential drawbacks before fully committing. Let’s consider a few of these concerns.

Infinite Banking Cons

Long-Term Commitment

While infinite banking offers the promise of financial freedom, it's not a quick fix. Building up a substantial cash value within your policy takes time, meaning you may not have immediate access to funds when you need them most. If you're looking for a solution to short-term financial challenges, infinite banking may not be the right fit.

Affordability Concerns

Another potential downside is the cost associated with whole life insurance policies. Financial advisors often recommend allocating around 10% of your yearly income towards these policies to fully leverage infinite banking. For many families, this amount may be financially burdensome and unsustainable in the long run.

Opportunity Cost

While infinite banking offers stable and predictable returns, it may come at the cost of missing out on potentially higher gains from other investment opportunities. Historically, the stock market has returned around 8% per year, whereas whole life insurance policies typically offer returns of 3-6% yearly. This means that if your primary goal is to maximize wealth accumulation through investments, other financial products or investment vehicles may be more suitable.

Lack of Immediate Liquidity

Since the cash value of your policy serves as collateral for loans, borrowing against it can limit your immediate access to funds. While you can access your cash value through policy loans, this process may take time and could be subject to certain restrictions or penalties.

Requires Complex Education

Implementing infinite banking requires a thorough understanding of the concept and its implications. You’ll need to invest in your financial knowledge or engage financial professionals to maximize the benefits of this strategy.

Setting Up and Qualifying for infinite banking

Every other day, someone sees updates like Brian's below and that sparks an immediate interest in infinite banking.

But without the right guidance, you may end up falling into pitfalls laid by brokers seeking commissions, risking your hard-earned savings. To keep you on the right path, here’s a guide through the process of setting up and qualifying for infinite banking policies, drawing from expert Nelson Nash's Becoming Your Own Banker.

Caption: Step-by-step checklist for setting up infinite banking

1. Assess Your Financial Situation

Evaluate your income, expenses, and long-term financial objectives to determine if infinite banking aligns with your needs. For example, suppose you're a young professional looking to build wealth over time. In that case, infinite banking could be a suitable strategy to consider as part of your long-term financial plan.

2. Find a Knowledgeable Advisor

To avoid being misled, seek advice from a financial advisor who understands the principles of infinite banking. They can help you through the complexities of setting up and managing your policy effectively.

3. Select a Whole Life Insurance Policy

Choose a participating whole life insurance policy that aligns with the infinite banking Concept. Look for policies with a track record of strong cash value growth and favorable loan terms, such as low-interest rates on policy loans.

To qualify for infinite banking, you need to have a whole life insurance policy with sufficient cash value. This usually requires consistent premium payments over some time.

4. Fund Your Policy

Start funding your policy with premium payments. Start funding your policy with premium payments. The goal is to build up the cash value over time, which you can then borrow against.

Calculating the implications of infinite banking helps you understand the potential returns and cash value growth of your policy over time. While there isn't a one-size-fits-all formula, your financial advisor can help you estimate the cash value growth based on factors such as premium payments, dividend rates, and policy loan interest rates.

This formula takes into account the premiums you've paid, the costs of insurance coverage, and any dividends or interest earned on your policy. It can give you an estimate of the cash value you can expect to accumulate over time. Remember, the actual cash value may vary based on the specific terms of the policy and the insurance company’s performance.

Tax Implications of infinite banking

When you borrow against your policy's cash value, the loan proceeds are generally not taxable This provides you with a tax-efficient way to access funds. But you need to understand the tax implications of policy loans and other aspects of infinite banking to maximize its benefits.

- Tax-Free Policy Loans

One of the significant advantages of infinite banking is accessing cash value through policy loans without triggering immediate tax consequences. For example, if your policy has a cash value of $100,000 and has grown to $150,000, you can take a tax-free loan of $50,000. This tax advantage can be a powerful tool in managing your finances and preserving wealth.

- Tax-Deferred Growth

Another tax benefit of infinite banking is the tax-deferred growth of the cash value within the policy. Unlike traditional investments where you may face annual taxes on gains, the growth within an infinite banking policy remains sheltered from taxes until you withdraw it. This tax-deferred growth can significantly enhance your overall returns over time.

While infinite banking offers tax advantages, one area of concern is the Modified Endowment Contract (MEC) status. If your policy becomes classified as an MEC due to excessive funding, withdrawals may be subject to taxes and penalties. Understanding the MEC rules and working closely with a financial advisor goes a long way in avoiding this potential issue.

Is the Infinite Banking concept legit?

We've all heard inspiring stories of people achieving financial freedom through infinite banking. Like how Walt Disney funded his dreams by borrowing against himself. But skepticism still exists. Interestingly, stoicism and infinite banking share a common thread—the idea that true freedom comes from within, whether it's emotional independence or financial autonomy.

So, Is the infinite banking concept legit? Let’s objectively examine both sides of the debate.

One major concern is the potential for high fees associated with whole life insurance policies, which can eat into the cash value growth over time. For example, if a policy has an annual fee of 1% of the cash value, a $100,000 policy could incur a $1,000 fee each year, impacting the overall cash value growth.

Infinite banking also requires a long-term commitment, and policyholders may not see significant benefits until several years into the policy.

Despite these legitimate concerns, many misconceptions exist about infinite banking.

One common myth is that it's a get-rich-quick scheme, which couldn't be further from the truth. For example, if someone expects to see substantial returns within a year of starting an infinite banking policy, they may be disappointed.

Another misconception is that it's only suitable for the wealthy. In reality, individuals of all income levels can benefit from the concept with proper planning and guidance.

Alternatives to infinite banking

While infinite banking offers unique benefits, such as tax advantages and control over your finances, it is not the only way to grow our financial assets. Want alternative options that may better suit your financial goals and risk tolerance? Here are a few:

- Traditional Savings Accounts: While they may offer lower interest rates, traditional savings accounts provide easy access to funds and are low risk.

- Certificates of Deposit (CDs): CDs offer higher interest rates than savings accounts but require locking your money for a specified period.

- Mutual Funds: Investing in mutual funds provides the opportunity for higher returns, but comes with market risks and fees.

- Real Estate Investments: Real estate can offer a hedge against inflation and potential for rental income, but requires significant capital and management.

- Stock Market Investments: Investing in stocks can provide high returns, but you’d have to consider market volatility and risk.

- 401(k) or IRA: These retirement accounts offer tax advantages and long-term growth potential. The downside is that these tend to have restrictions on withdrawals and contribution limits.

| Financial Product | Tax-Free Growth | Access to Cash Value | Market Risk | High Growth Potential |

| infinite banking | Yes | Yes | No | No |

| Savings Accounts | No | Yes | No | No |

| Certificates of Deposit | No | Yes | No | No |

| Mutual Funds | No | Yes | Yes | Yes |

| Real Estate | No | No | Yes | Yes |

| Stock | No | No | Yes | Yes |

| 401(k) or IRA | Yes | Limited | Yes | Yes |

Safely Grow and Leverage Your Capital with infinite banking

Infinite banking addresses a fundamental issue in personal finance: the need to finance everything we buy. Whether through traditional financing or using cash, we often surrender the potential future growth of our capital. Infinite banking offers a solution by giving each dollar multiple jobs, allowing you to safely grow and leverage your capital in ways that traditional banking can only dream of.

If you're interested in learning more about how infinite banking can switch up your financial future, consider enrolling in my financial education course. You’ll enjoy comprehensive insights into infinite banking and other wealth-building strategies, so you can take control of your finances.