The CD ladder strategy is one of my favorite ways to boost savings yield without giving up too much flexibility.

Here's how to fast-track building a CD ladder that actually works for your goals, in less then ten minutes (watch the video if you only want the overview).

Quick Refresher: What’s a CD Ladder?

A CD ladder is a simple but powerful setup where you split your money across multiple CDs with staggered maturity dates. It’s like having a steady flow of your savings coming back to you – plus the bonus of locking in higher interest rates on longer CDs.

Why Bother With a CD Ladder?

Steady cash flow: Instead of tying up all your cash in one long-term CD, a ladder gives you regular access to your money as CDs mature.

Rate protection: Interest rates go up and down. With a ladder, you’re “averaging” your way in – some CDs get better rates, some might be a little lower, but overall, you’re smoothing things out.

More earnings vs. savings accounts: You’ll usually beat even high-yield savings accounts, especially if rates are trending up.

The Data-Backed Advantage: Laddering vs. Plain CDs

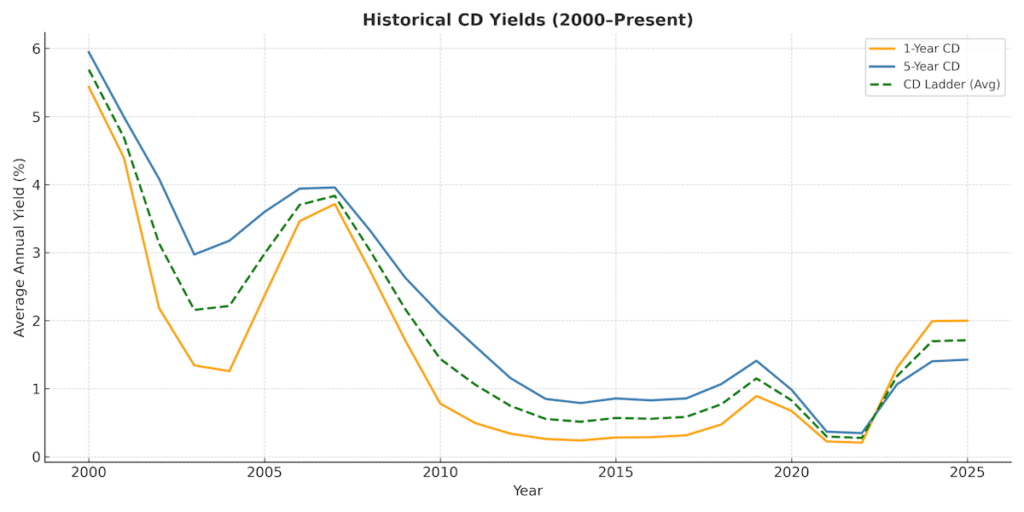

Here’s the kicker: Historical data shows that CD ladders actually earn almost as much as just rolling 5-year CDs – and way more than sticking with 1-year CDs.

Average APYs (2000–2025)

| Investment Strategy | Average APY |

| 1-year CD | ~1.7% |

| 5-year CD | ~2.6% |

| 5-year CD ladder | ~2.4% |

So over the long term, laddering delivered a yield about 1% higher than rolling 1-year CDs – without tying up all your money for 5 years. Compared to rolling 5-year CDs, ladders only missed out by ~0.2% on average – a tiny tradeoff for having annual access to your cash!

This makes laddering a sweet spot: most of the yield upside of long-term CDs, plus the flexibility to re-evaluate your plan every year.

Three CD Ladder Structures (Choose Based on Your Goal)

1. The Emergency Fund Ladder

- Goal: Access cash if you need it, but earn a bit more than a savings account.

- Setup:

- Divide your emergency fund into four equal parts.

- Put each part in a 3-month, 6-month, 9-month, and 12-month CD.

- Every three months, one CD matures – if you don’t need the cash, roll it over.

- Why it’s smart: Always have money coming back to you in case of a real emergency.

2. The Yield Maximizer Ladder

- Goal: Long-term yield (good for retirees or folks with a solid emergency stash elsewhere).

- Setup:

- Split your money into 5 equal chunks.

- Invest in 1, 2, 3, 4, and 5-year CDs.

- As each CD matures, roll it back into a 5-year CD for top rates.

- Why it’s smart: You’re always locking in the best long-term rates, but still get some cash flow each year.

3. The Flexibility Hedge Ladder

- Goal: Not sure what the future holds? Hedge your bets.

- Setup:

- Mix of short-term (6–12 month) and longer-term (2–3 year) CDs.

- Keep some money liquid-ish, and some earning a bit more.

- Why it’s smart: A good balance for folks who might have big purchases down the road but want to earn more while waiting.

Building Your CD Ladder: The No-Nonsense Steps

- Decide how much cash you’re comfortable locking up.

- Pick your ladder structure based on your goal.

- Open CDs in staggered terms at your bank or credit union.

- Set up auto-rollover if your bank allows it (makes life easier!).

- Revisit your ladder once a year or if rates shift by a full percent or more.

The “Ladder Health Check” You Shouldn’t Skip

Here’s a key step most folks miss: checking in on your ladder every year. Rates change, your cash needs change – and it’s easy to let your ladder get stale.

Annual review checklist:

- Are rates significantly different?

- Has your emergency fund situation changed?

- Do you need more or less cash flow in the next year?

Doing this keeps your ladder working for you, not the other way around.

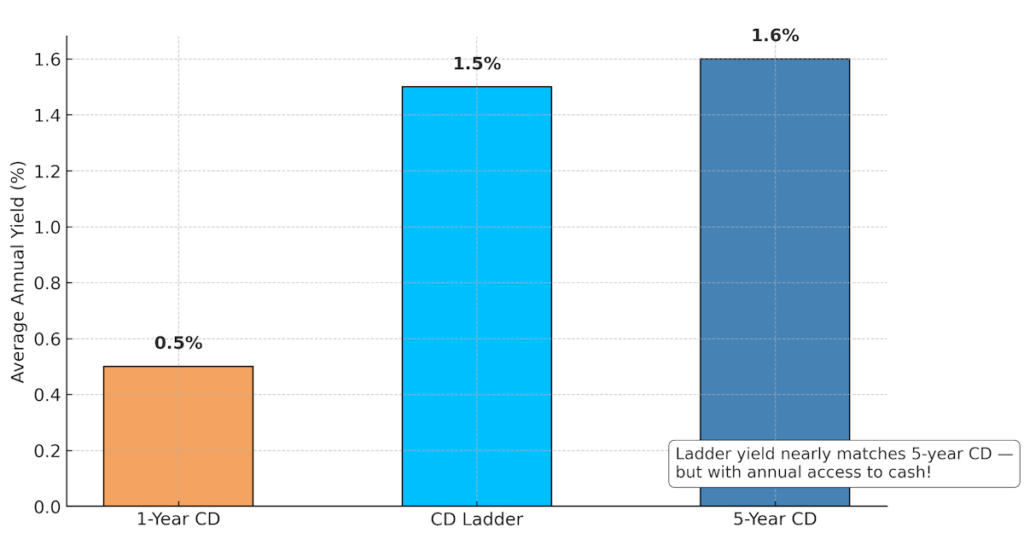

Real-World Example: How Laddering Beat 1-Year CDs

Between 2010 and 2015, 1-year CDs were paying an average of ~0.5% – but laddered CDs were averaging ~1.5% during that same period. That’s 3x higher yield, without taking on extra risk or locking away all your funds for 5 years.

It’s a small but steady edge that adds up over time.

Watch Out For These Gotchas

- Early withdrawal penalties: Don’t lock up money you know you might need soon.

- Overcomplicating it: You don’t need 12 CDs to ladder! 3–5 CDs are fine for most folks.

- Ignoring tax impact: CD interest is taxable as income. Don’t forget to plan for it.

So, Is a CD Ladder Right for You?

If you’ve got cash you know you won’t need all at once – and you want to earn a little more without the stress of the markets – a CD ladder can be a smart move.

If you’re still not sure, ask yourself:

- “How important is it to have cash flow every few months?”

- “Am I okay earning a bit more in exchange for a little less flexibility?”

Next Steps: Take Action Now

Check your bank’s CD rates and see what’s on offer today. Sketch out a quick ladder plan based on your goal – emergency fund, yield maximizer, or flexibility hedge. Set it up and automate rollovers.

If you found this helpful, check out my course on personal finance mastery – highly-rated by hundreds of students for the actionable strategies I share. Lessons I learned through years of trial and error to take me from $70K in debt to being complete financial freedom and being semi-retired at forty.